Unlocking Your Future: A Comprehensive Guide to Roth IRAs

Planning for retirement can feel like navigating a maze, especially when it comes to understanding the financial tools at your disposal.

One such tool that often garners interest, yet remains shrouded in complexity, is the Roth IRA.

In this blog post, we aim to demystify the Roth IRA, breaking it down to its basics, and discussing its benefits, contribution limits, and why it might be an ideal choice for your retirement savings.

As a trusted partner in your financial journey, Riverside Capital Management Group will guide you through each step, showing you how this powerful tool can be integrated into your financial strategy and managed effectively to secure your future.

How does it work? It's simple. You contribute a certain amount of your after-tax income to this account every year. This money then gets invested, often in a mix of stocks, bonds, and mutual funds.

Over time, these investments have the opportunity to grow, and thanks to the nature of the Roth IRA, the growth is tax-advantaged. This allows the money to compound over the years, building a substantial nest egg for your retirement.

Since you contribute to a Roth IRA with after-tax dollars, distributions during retirement are typically not taxed. This means you have a better idea of how much money you will have during your retirement years. However, this can get complicated. The IRS rules around distributions from a Roth IRA are fraught with specifics, depending on the status of each account and each owner. It pays to fully understand the rules, which will be discussed in more depth in a later section. For now let’s look at the two main types of distributions: qualified and non-qualified.

Qualified distributions, which are tax-free and not included in gross income, occur when your account has been open for more than five years and you are at least 59 ½, or as a result of your death, disability, or using the first-time homebuyer exemption.

The five-year waiting period for qualified Roth IRA distributions begins for all of your Roth IRAs on January 1 of the first taxable year for which the amount was funded and ends on December 31 of the fifth year.

Nonqualified distributions, on the other hand, do not meet the above requirements. However, this does not necessarily mean that nonqualified distributions are included in gross income.

Furthermore, if your spouse is the Roth IRA beneficiary, they will not have RMDs if they roll over or transfer the Roth IRA and treat it as their own. This allows for an additional period of tax-free compounding of potential earnings that can help grow your family’s wealth.

Beneficiaries can distribute earrings tax-free from an Inherited Roth IRA as long as the Roth had been funded for more than five years. Most non-spouse beneficiaries will need to empty their inherited Roth IRA by the 10th year following the year of the Roth IRA owner’s death. No distributions are required before the 10th year.

This flexibility can be especially beneficial during financial emergencies when you might need to access your funds.

Strategically, a Roth IRA can complement other qualified retirement accounts (QRPs) like 401(k)s and traditional IRAs, providing a mix of taxable and tax-free income in retirement.

Importantly, early and consistent contributions to a Roth IRA can significantly impact your retirement savings.

The more time your investment has to grow, the more you can benefit from the power of compound interest. This can potentially lead to a sizable nest egg in retirement. Hence, incorporating a Roth IRA into your retirement plan early and maintaining regular contributions are key steps in maximizing your retirement savings.

It begins with a simple consultation with financial professionals who will assess your financial situation, goals, and risk tolerance. This information helps them guide you in setting up a Roth IRA that aligns with your retirement planning objectives.

Once the initial consultation is complete, the advisors will assist you in completing the necessary paperwork to establish your Roth IRA account.

The advisor should walk you through every step of the process, ensuring you understand your contribution limits, tax implications, and withdrawal rules.

After your account is set up, the advisor provides ongoing management and advice with an approach that is designed to optimize your Roth IRA's potential while minimizing risk.

You will want to choose a company who can explain withdrawal rules and tax implications of income distribution in retirement, amongst other essential services.

educational information to help you understand all the ends and outs of planning for your future. These are both positive implications that the firm will have the expertise to navigate the complexities of wealth planning, including the strategic use of Roth IRAs, to ensure you're well-positioned for a comfortable and secure retirement.

Do your homework and look for a partner that you can trust in helping you achieve your financial milestones. Select a firm that goes beyond just managing your Roth IRA.

Ask how they create personalized investment planning strategies that integrate Roth IRAs effectively. After all, you deserve unwavering commitment to your financial well-being.

Understanding Roth IRAs and their role in retirement planning can be a complex process, but it doesn't have to be a daunting task.

With the right guidance and personalized financial strategy, this powerful financial tool can be leveraged effectively to secure a comfortable retirement.

Riverside Capital Management Group is committed to helping you navigate this financial journey, bringing its extensive knowledge in managing Roth IRA accounts to the table.

Our dedication extends beyond simply managing your Roth IRA. We work closely with our clients to understand their overall financial picture and provide comprehensive wealth planning.

This includes assessing risk tolerance, understanding short and long-term objectives, and crafting a custom strategy designed to optimize wealth growth and preservation.

We take into account your financial goals, risk tolerance, and retirement timeline, amongst other considerations. This personalized approach ensures that your Roth IRA isn't just a standalone account but is a key component of your comprehensive investment plan.

Remember, the earlier and more consistent your contributions, the greater your potential for growth and tax-free income during your retirement years. Invest in your future with Riverside Capital Management Group - we're here to help to ensure your financial success.

Embrace the benefits of a Roth IRA today and take the first step towards secure retirement savings. Our team of financial professionals is ready to guide you in setting up your Roth IRA and developing a strategy that aligns with your financial goals. Contact Riverside CMG today to get started.

This article was written by Redstitch, LLC and provided to you by Riverside Capital Management Group.

Wells Fargo Advisors Financial Network is not a legal or tax advisor.

One such tool that often garners interest, yet remains shrouded in complexity, is the Roth IRA.

In this blog post, we aim to demystify the Roth IRA, breaking it down to its basics, and discussing its benefits, contribution limits, and why it might be an ideal choice for your retirement savings.

As a trusted partner in your financial journey, Riverside Capital Management Group will guide you through each step, showing you how this powerful tool can be integrated into your financial strategy and managed effectively to secure your future.

Understanding the Roth IRA

A Roth IRA, named after Senator William Roth who spearheaded its creation, is an individual retirement account that offers a unique advantage: tax-free growth potential.How does it work? It's simple. You contribute a certain amount of your after-tax income to this account every year. This money then gets invested, often in a mix of stocks, bonds, and mutual funds.

Over time, these investments have the opportunity to grow, and thanks to the nature of the Roth IRA, the growth is tax-advantaged. This allows the money to compound over the years, building a substantial nest egg for your retirement.

3 Benefits of a Roth IRA

A Roth IRA brings multiple benefits that may make it an appealing choice for your retirement savings.1) “Income-tax Free” Distributions

One of the most significant advantages is because of the focus on “income-tax free” distributions that are available.Since you contribute to a Roth IRA with after-tax dollars, distributions during retirement are typically not taxed. This means you have a better idea of how much money you will have during your retirement years. However, this can get complicated. The IRS rules around distributions from a Roth IRA are fraught with specifics, depending on the status of each account and each owner. It pays to fully understand the rules, which will be discussed in more depth in a later section. For now let’s look at the two main types of distributions: qualified and non-qualified.

Qualified distributions, which are tax-free and not included in gross income, occur when your account has been open for more than five years and you are at least 59 ½, or as a result of your death, disability, or using the first-time homebuyer exemption.

The five-year waiting period for qualified Roth IRA distributions begins for all of your Roth IRAs on January 1 of the first taxable year for which the amount was funded and ends on December 31 of the fifth year.

Nonqualified distributions, on the other hand, do not meet the above requirements. However, this does not necessarily mean that nonqualified distributions are included in gross income.

2) Required Minimum Distributions (RMDs)

Another advantage is the absence of required minimum distributions (RMDs). Unlike traditional IRAs, which mandate distributions at retirement age, with Roth IRAs, you do not have to take required minimum distributions (RMDs) during your lifetime, optimizing the opportunity to build tax-free wealth.Furthermore, if your spouse is the Roth IRA beneficiary, they will not have RMDs if they roll over or transfer the Roth IRA and treat it as their own. This allows for an additional period of tax-free compounding of potential earnings that can help grow your family’s wealth.

Beneficiaries can distribute earrings tax-free from an Inherited Roth IRA as long as the Roth had been funded for more than five years. Most non-spouse beneficiaries will need to empty their inherited Roth IRA by the 10th year following the year of the Roth IRA owner’s death. No distributions are required before the 10th year.

3) Distribution Rule Flexibility

Finally, a Roth IRA provides flexibility in distribution rules. For instance, you may take a distribution of contributions (but not earnings) at any time without penalty, offering a degree of liquidity not often seen in retirement accounts.This flexibility can be especially beneficial during financial emergencies when you might need to access your funds.

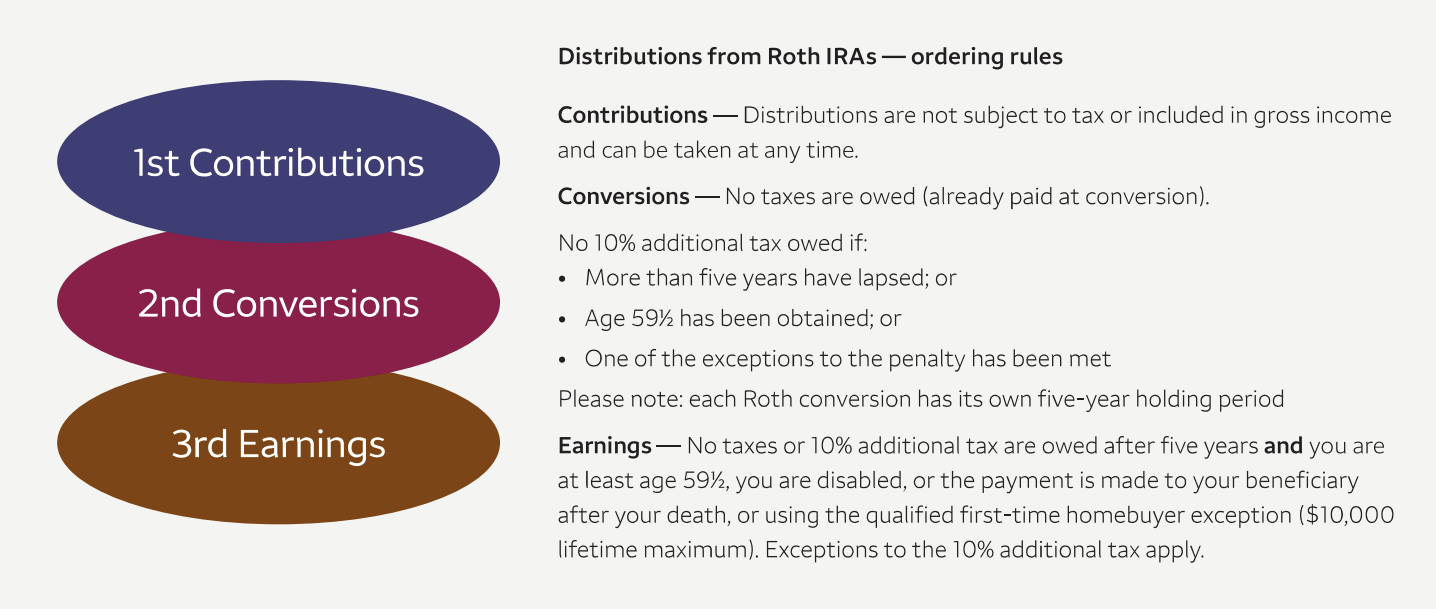

Getting to Know the Roth IRA Distribution Rules

Unlike Traditional IRAs, there are ordering rules when taking nonqualified distributions from a Roth IRA. As mentioned early, this can make things complicated. Here is a break-down of the rules to give you the complete picture:- Contributions come first - The first amounts distributed from any of your Roth IRAs, if you have several accounts, are annual contributions. Because Roth contributions are not deductible, they are not subject to tax or included in gross income and can be taken anytime.

- Converted dollars are next - After you have exhausted all of your contributions, the next amounts distributed are from any conversions you have completed. These conversion amounts are distributed tax-free on a first in, first out basis. Converted amounts taken before the five-year holding period, or you are age 59 ½ or older, whichever is first, may have a 10% additional tax, unless an exemption applies.

- Earnings are last - The last money is distributed from earnings. Earnings taken before the account has been open for longer than five years and you are at least 59 ½ or older, or you are disabled, or the payment is made to your beneficiary after your death, or using the first-time homebuyer exemption, are subject to income tax and the 10% additional tax, unless another exemption applies.

- Exemptions to the 10% additional tax - The exemptions include distributions after reaching age 59 ½, death, disability, eligible medical expenses, certain unemployed individual’s health insurance premiums, qualified first-time homebuyer ($10,000 lifetime maximum), qualified higher education expenses, Substantially Equal Periodic Payments (SEPP), Roth conversion, qualified reservist distribution, qualified birth or adoption expenses, or IRS levy.

Comparing Roth IRA to Traditional IRA

A Roth IRA and a traditional IRA have distinct differences that make each one appropriate for different financial goals and situations. When analyzing which type is right for you, one key decision point is when you want to pay income taxes on your savings.Tax Benefits

One of the most significant distinctions lies in their tax benefits. While a Roth IRA allows for tax-free growth potential, whereas traditional IRAs offer tax-deferred growth potential.- Roth IRA - Pay taxes now - Investment earnings are distributed tax-free, (based on the distribution rules discussed earlier). Since contributions to a Roth IRA are not deductible, there is no tax deduction regardless of income. If your income exceeds the modified adjusted gross income (MAGI) limit, you are not eligible to contribute to a Roth IRA.

- Traditional IRA - Pay taxes later - You pay no taxes on any investment earnings until you distribute the money from your account, presumably in retirement. Additionally, depending on your income, your contribution may be tax deductible. Deferring taxes allows for a potentially greater accumulation of wealth.

Eligibility

The eligibility criteria for each type also vary. Traditional IRAs have no income limits for contributors, while Roth IRAs are only available to individuals and couples within certain income thresholds.Distribution Rules

Distribution rules are another area of contrast. Roth IRAs offer more flexibility, allowing for tax-free and penalty-free distributions of contributions at any time. On the other hand, traditional IRAs impose a 10% additional tax if funds are withdrawn before the age of 59 ½, barring certain exemptions.The Role of Roth IRA in Retirement Planning

A Roth IRA plays a crucial role in retirement planning due to its unique tax advantages and flexible distribution rules. It serves as a valuable component in a diversified portfolio, offering a balance between risk and reward.Strategically, a Roth IRA can complement other qualified retirement accounts (QRPs) like 401(k)s and traditional IRAs, providing a mix of taxable and tax-free income in retirement.

Importantly, early and consistent contributions to a Roth IRA can significantly impact your retirement savings.

The more time your investment has to grow, the more you can benefit from the power of compound interest. This can potentially lead to a sizable nest egg in retirement. Hence, incorporating a Roth IRA into your retirement plan early and maintaining regular contributions are key steps in maximizing your retirement savings.

Getting Started with Your Roth IRA

Opening a Roth IRA is a pretty straightforward process.It begins with a simple consultation with financial professionals who will assess your financial situation, goals, and risk tolerance. This information helps them guide you in setting up a Roth IRA that aligns with your retirement planning objectives.

Once the initial consultation is complete, the advisors will assist you in completing the necessary paperwork to establish your Roth IRA account.

The advisor should walk you through every step of the process, ensuring you understand your contribution limits, tax implications, and withdrawal rules.

After your account is set up, the advisor provides ongoing management and advice with an approach that is designed to optimize your Roth IRA's potential while minimizing risk.

3 Things to Look for in A Dedicated Financial Firm

Selecting the right financial advisor plays a pivotal role in getting proper assistance in setting up a Roth IRA.Specializes in IRA Setup

Look for a company who has a team of dedicated professionals with a wealth of knowledge in setting up and managing Roth IRA accounts. This includes setting up the account, determining contribution limits and eligibility criteria based on individual financial situations.You will want to choose a company who can explain withdrawal rules and tax implications of income distribution in retirement, amongst other essential services.

Years of Experience

Look for a firm who has years of experience and a resource section that supplies ampleeducational information to help you understand all the ends and outs of planning for your future. These are both positive implications that the firm will have the expertise to navigate the complexities of wealth planning, including the strategic use of Roth IRAs, to ensure you're well-positioned for a comfortable and secure retirement.

Longevity with Customers

Ask any potential companies how they work to foster strong, long-term relationships with their clients. Ask about their methods of communication and any personalized service offerings they have available.Do your homework and look for a partner that you can trust in helping you achieve your financial milestones. Select a firm that goes beyond just managing your Roth IRA.

Ask how they create personalized investment planning strategies that integrate Roth IRAs effectively. After all, you deserve unwavering commitment to your financial well-being.

Don’t Wait for Tomorrow, Start Planning Your Future Today!

A Roth IRA provides a flexible way to build retirement assets, to provide future income, or to potentially accumulate significant funds for your heirs.Understanding Roth IRAs and their role in retirement planning can be a complex process, but it doesn't have to be a daunting task.

With the right guidance and personalized financial strategy, this powerful financial tool can be leveraged effectively to secure a comfortable retirement.

Riverside Capital Management Group is committed to helping you navigate this financial journey, bringing its extensive knowledge in managing Roth IRA accounts to the table.

Our dedication extends beyond simply managing your Roth IRA. We work closely with our clients to understand their overall financial picture and provide comprehensive wealth planning.

This includes assessing risk tolerance, understanding short and long-term objectives, and crafting a custom strategy designed to optimize wealth growth and preservation.

We take into account your financial goals, risk tolerance, and retirement timeline, amongst other considerations. This personalized approach ensures that your Roth IRA isn't just a standalone account but is a key component of your comprehensive investment plan.

Remember, the earlier and more consistent your contributions, the greater your potential for growth and tax-free income during your retirement years. Invest in your future with Riverside Capital Management Group - we're here to help to ensure your financial success.

Embrace the benefits of a Roth IRA today and take the first step towards secure retirement savings. Our team of financial professionals is ready to guide you in setting up your Roth IRA and developing a strategy that aligns with your financial goals. Contact Riverside CMG today to get started.

This article was written by Redstitch, LLC and provided to you by Riverside Capital Management Group.

Wells Fargo Advisors Financial Network is not a legal or tax advisor.